Existing Home Sales

612-382-4099

For Week Ending December 14, 2024

For Week Ending December 14, 2024

For the first time in 10 years, the U.S. real median gross cost of renting—rent, plus the average monthly cost of utilities and fuel, adjusted for inflation—grew faster than median home values on an annual basis in 2023, rising 3.8% compared to 1.8%, according to the 2023 American Community Survey. The median gross rent rose from $1,354 in 2022 to $1,406 in 2023, with renters spending 31% of their income on rent and utilities.

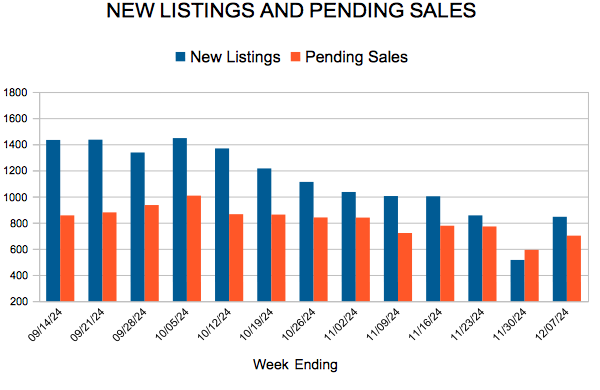

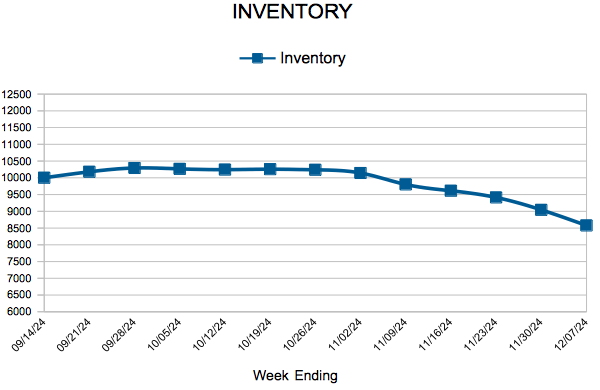

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING DECEMBER 14:

FOR THE MONTH OF NOVEMBER:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

December 19, 2024

This week, mortgage rates crept up to a similar average as this time in 2023. For the most part, mortgage rates have moved between 6 and 7 percent over the last 12 months. Homebuyers are slowly digesting these higher rates and are gradually willing to move forward with buying a home, resulting in additional purchase activity.

Information provided by Freddie Mac.

(Dec. 17, 2024) – According to new residential market data from the Minnesota state and Twin Cities metro REALTOR® associations, sales, prices and inventory all rose in November while seller activity was down slightly.

Sellers, Buyers and Housing Supply

With 11 months in the books so far, we’re getting a clear picture of how the 2024 housing market performed relative to past years. For November, pending sales statewide rose for a second month in a row while new listings showed their first decline in three months. Five out of 14 regions across the state saw year-over-year gains in new listings while 8 of 14 regions saw year-over-year increases in pending sales. All 14 regions saw rising home prices compared to last November. Twelve of 14 regions showed inventory growth from last year. The biggest gain in new listings was in the Alexandria region; the largest increase in pending sales was in the Detroit Lakes region; the largest jump in home prices was in the Grand Rapids area. St. Cloud was the tightest and most undersupplied market. The Twin Cities metro is the highest priced area and accounts for 66.3% of statewide sales activity and 60.2% of statewide inventory.

Buyers remain rate-sensitive, though perhaps less than in the recent past. In November, the 30-year mortgage rate averaged its highest level since July of this year. Despite that, statewide pending sales rose 8.5%, their second largest increase in eight months. This could signify a growing acceptance of the current rate environment. There’s also a high degree of pent-up demand to make a move. But listings declined 0.9% in November, which was essentially flat. The Federal Reserve is likely to cut its benchmark rate this month, but the Fed could be slower to cut rates in 2025. That means mortgage rates are still likely to come down, but at a slower pace than anticipated. While that should help with affordability, there are concerns about whether rising insurance rates and property taxes could negate any progress. It’s still worth noting that wage growth has been exceeding the rate of inflation. Slower growth in home prices combined with strong wage growth could also help improve affordability without home prices falling.

“We’re at a time of year when buyers can take advantage of a slower pace and a calmer, less competitive environment,” said Geri Theis, President of Minnesota Realtors®. “My buyers in beautiful southeastern Minnesota are enjoying the fact that we have the most inventory since 2019.”

On the active supply side, inventory levels rose 3.9% compared to last November. That indeed puts the current inventory figure at its highest level for any November since 2019—yet still 26.7% below that level. While buyers can take some comfort in that, it’s still important to recognize the ongoing supply shortage, despite recent inventory growth across the state and metro. The residential marketplace continues to rebalance and normalize. Every month this year has had a higher month’s supply of inventory compared to 2023. But the triple punch of higher prices, higher interest rates and low supply is still hindering would-be buyers.

Prices, Market Times and Negotiations

Every location and market segment is unique. Some listings fetch multiple offers and close for over list price while other sellers are accepting offers below asking price. Overall, sellers accepted 96.7% of their original list price statewide and 97.6% in the metro—both more or less flat from last year. And those offers were accepted after an average of 45 days on market statewide and 50 days in the metro—both figures up from a year ago.

“I see buyers showing more interest yet also being more cautious,” said Jamar Hardy, President of Minneapolis Area REALTORS®. “And part of that is that they’re slowly but surely seeing more options hit the marketplace. Minneapolis and the surrounding suburbs in particular offer a wide array of housing options across the entire price spectrum.”

The statewide median home price was up 4.4% to $340,000 while the Twin Cities price was up 3.4% to $375,000. Aside from more choices for buyers, improved housing supply should also translate to less upward price pressure and thus more modest price growth. All real estate markets are local. A few hours north of Minneapolis, the median home price in Grand Rapids rose nearly 30.0% but stood at $270,000. Just 40 minutes east of there—in the heart of the Iron Range—the median price was $160,000 in the Hibbing and Virginia area. And homes two hours west of Minneapolis in the Willmar area are selling for around $215,000. In Rochester, just over an hour southeast of the Twin Cities, home prices are closer to $285,000. These November figures are always lower than their summer highs but are all higher than a year ago.

“Many buyers and sellers are feeling renewed optimism about making a move and are returning to the market,” said Amy Peterson, President of the Saint Paul Area Association of REALTORS®. “Realtors are engaging in meaningful conversations about the full scope of homeownership costs, and buyers are growing more comfortable with current interest rates. By understanding the unique goals and options of each buyer and seller, we can provide thoughtful guidance and tailor solutions to help them navigate today’s challenging market conditions.”

Locational Differences | Minnesota statewide

Market activity always varies by area, price point and property type. Regions such as Alexandria, Mankato and Brainerd saw the largest gains in seller activity. St. Cloud, Willmar and Rochester had the largest gains in pending sales. Homes sold the fastest in the Duluth/North Shore region along with St. Cloud and Rochester. Prices were highest in the Twin Cities followed by Detroit Lakes and Brainerd. The most affordable regions of the state were Hibbing/Virginia and Willmar. Every region is undersupplied except Bemidji, which is relatively well balanced.

Locational Differences | Twin Cities Metro

For cities with at least five sales, Maple Lake, Hanover and Chisago had the largest sales gains. The highest priced areas were North Oaks, Medina and Orono while the most affordable areas were Little Canada, Pine City and Lonsdale. Homes sold the quickest in Ham Lake, Lonsdale and Spring Lake Park but took the longest to sell in Columbus, Hanover and North Oaks. The most undersupplied markets were St. Bonifacius, Richfield and North St. Paul while the most oversupplied markets were Hanover, Cologne and Scandia.

From The Skinny Blog.

For Week Ending December 7, 2024

For Week Ending December 7, 2024

The Federal Housing Finance Agency recently announced the conforming loan limits for one-unit properties with mortgages acquired by Fannie Mar and Freddie Mac will be $806,500 in 2025, an increase of $39,950 (5.2%) from 2024’s ceiling of $766,550. However, in high-cost areas where 115% of the local median home value exceeds the baseline conforming loan limit value, the new loan limit for one-unit properties will be $1,209,750.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING DECEMBER 7:

FOR THE MONTH OF NOVEMBER:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.