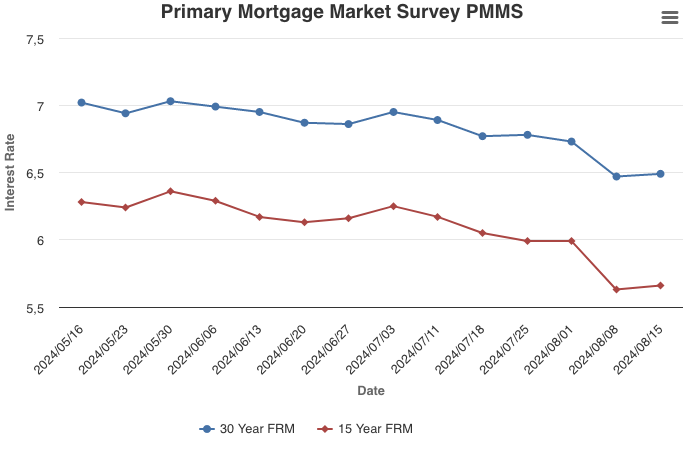

August 15, 2024

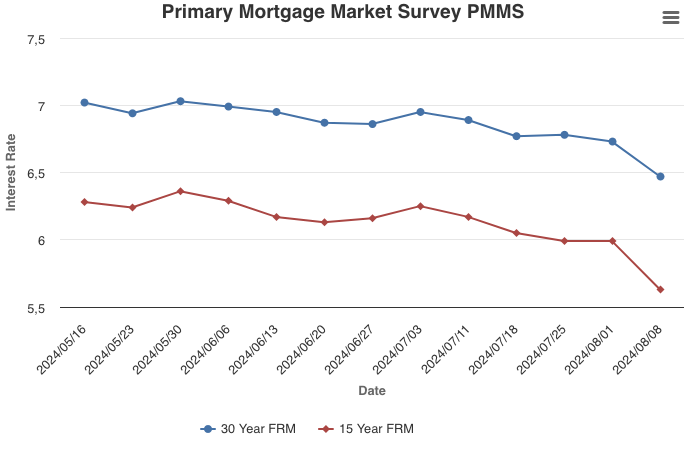

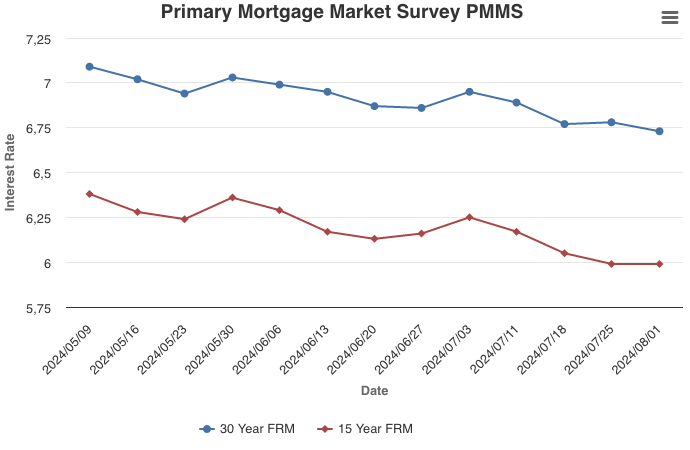

While rates increased slightly this week, they remain more than half a percent lower than the same time last year. In 2023, the 30-year fixed-rate mortgage nearly hit 8 percent, slamming the brakes on the housing market. Now, the 30-year fixed-rate hovers around 6.5 percent and will likely trend down in the coming months as inflation continues to slow. Lower rates are good news for potential buyers and sellers alike.

Information provided by Freddie Mac.

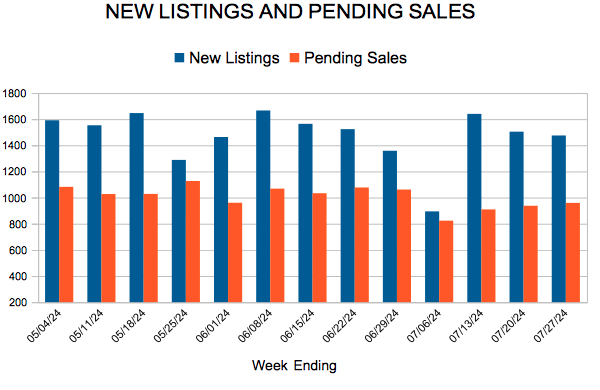

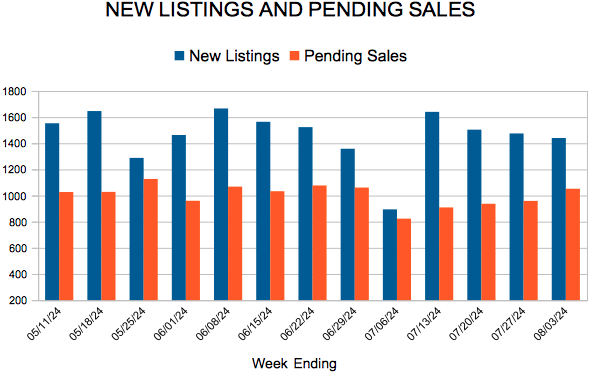

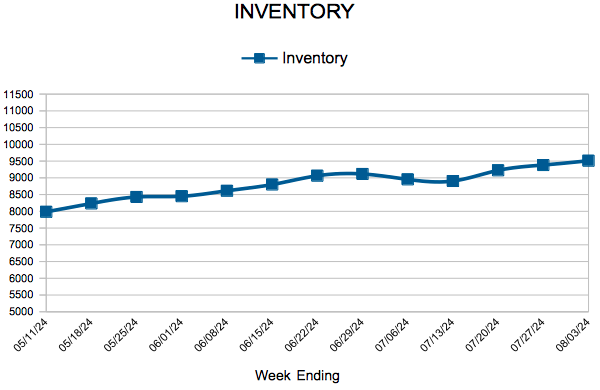

For Week Ending August 3, 2024

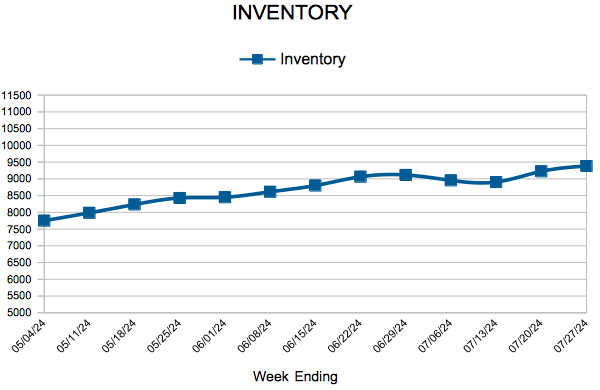

For Week Ending August 3, 2024