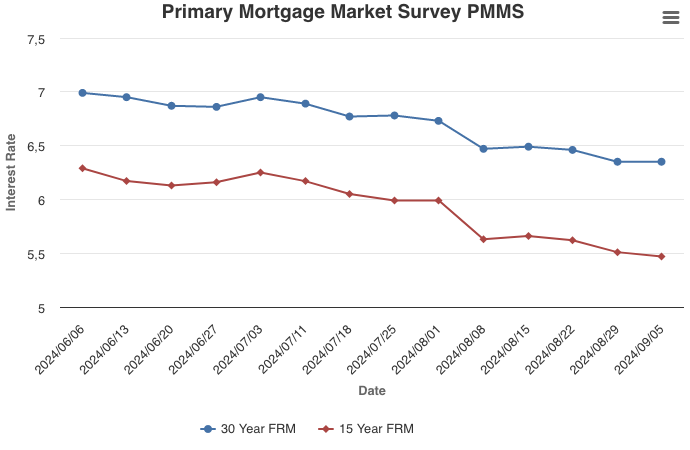

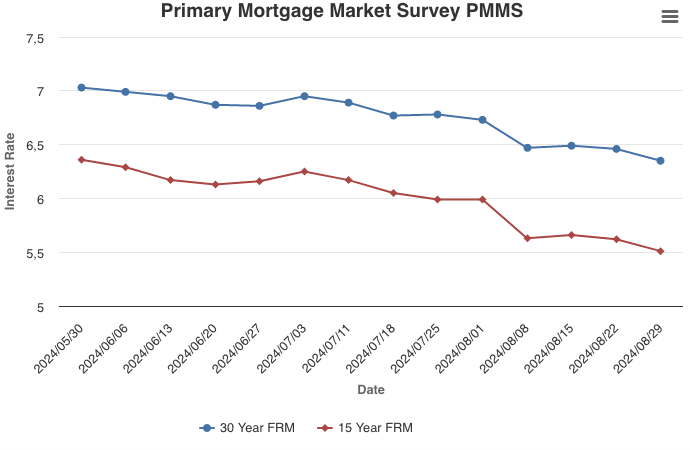

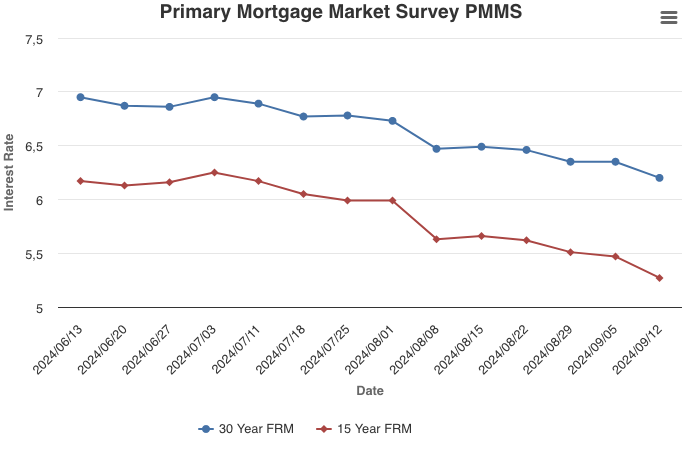

September 12, 2024

Mortgage rates have fallen more than half a percent over the last six weeks and are at their lowest level since February 2023. Rates continue to soften due to incoming economic data that is more sedate. But despite the improving mortgage rate environment, prospective buyers remain on the sidelines, as they negotiate a combination of high house prices and persistent supply shortages.

Information provided by Freddie Mac.

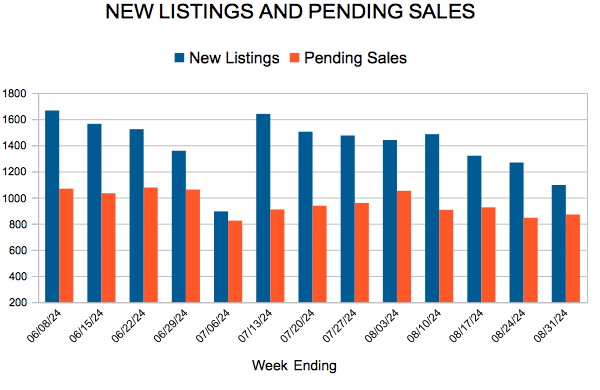

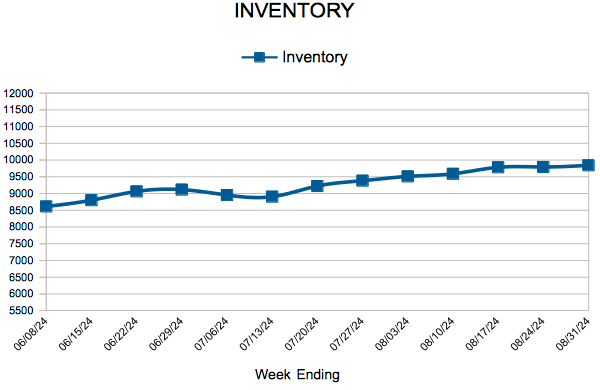

For Week Ending August 31, 2024

For Week Ending August 31, 2024